Forensic accounting

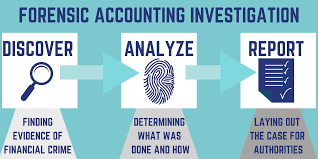

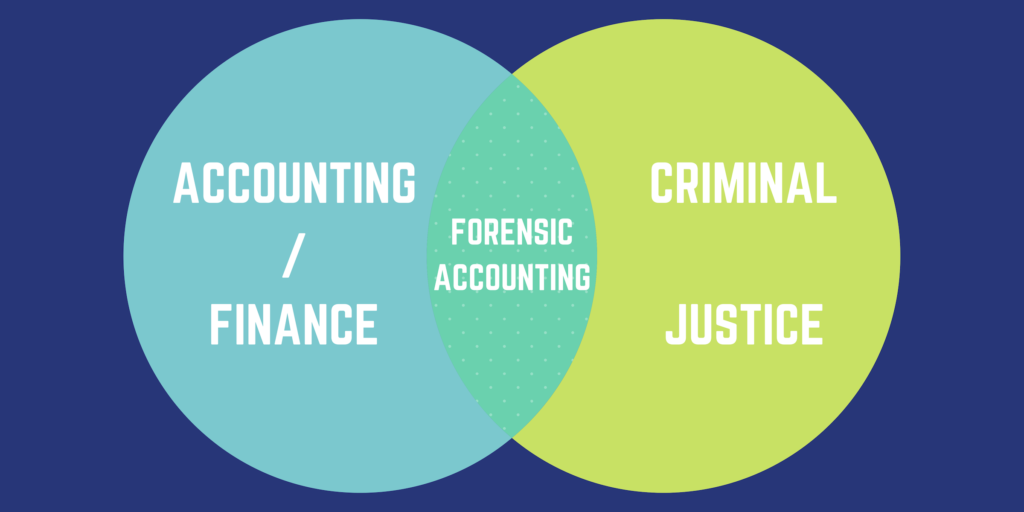

Forensic accounting is the investigation of fraud or misinterpretation. It involves different techniques and skills like accounting and auditing to conduct an examination into the finances of an individual or business while providing an analysis suitable to be used in legal proceedings.

This process is carried out by a team of professionals trained to look beyond the numbers and deal with the business reality of a situation. As forensic accounting is often used in fraud or embezzlement cases to explain the nature of a financial crime, the team is responsible for carrying out the following tasks:

- Collecting evidence pertaining to hidden assets

- Interviewing associated parties and employees

- Verifying and analyzing collected data

- The conclusions are then summarized into reports and the evidence is bundled into exhibits to be presented in a court of law.

Forensic accounting has been divided into two categories:

- Litigation support

- Investigation and dispute resolution

Litigation support entails the presentation and interpretation of a variety of topics based on assisting ongoing or pending litigation. Issues related to the quantification of economic damages involve this type of forensic accounting.

Investigation and dispute resolution are the second type of forensic accounting. It is a step in determining whether criminal offences such as employee theft, securities fraud, identity theft, and insurance fraud have happened. A forensic accountant’s job may include making recommendations for steps that might be taken to reduce future losses and damages. Investigations can be carried out in civil matters as well varying from hidden assets in a divorce case to theft.

As seen, forensic accounting is emerging as a field of knowledge with many applications. Therefore, it adopts a new method to understand forensic accounting as an education as well as a profession.